New Jersey Health Insurance Costs and Savings

Understand what you’ll pay for coverage in 2026, discover premium tax credits and state subsidies, and learn proven strategies to reduce your healthcare expenses.

Understanding New Jersey Health Insurance Costs

Health insurance costs in New Jersey consist of several components that together determine what you actually pay for coverage. Understanding how these pieces fit together helps you compare plans accurately and avoid surprises when you need care.

For 2026, New Jersey marketplace premiums have increased an average of 16.6% compared to the prior year. This increase reflects rising healthcare costs, higher pharmacy expenses, and changes to federal subsidy programs. However, most residents qualify for financial assistance through GetCoveredNJ that significantly reduces these amounts. New Jersey also offers state-funded subsidies extending to households earning up to 600% of the Federal Poverty Level, providing additional relief beyond federal assistance.

Components of Health Insurance Costs

When evaluating health insurance options, you’ll encounter several cost categories. Each affects your total annual spending differently depending on how much healthcare you use.

Monthly Premium

The amount you pay each month to maintain coverage, regardless of whether you use any healthcare services. This is your fixed cost for having insurance.

Annual Deductible

The amount you pay out-of-pocket before insurance begins paying. With a $3,000 deductible, you pay the first $3,000 of covered expenses yourself.

Copayments

Fixed amounts for specific services, such as $30 for a primary care visit or $50 for a specialist. Copays often apply after meeting your deductible.

Coinsurance

Your share of costs after meeting your deductible, expressed as a percentage. With 20% coinsurance, you pay 20% while insurance covers 80%.

Out-of-Pocket Maximum

The most you’ll pay in a plan year. Once reached, insurance covers 100% of additional care. For 2026, the federal max is $9,450 individual / $18,900 family.

Prescription Costs

Drug costs vary by formulary tier. Generic drugs cost less than brand-name. Check if your medications are covered and at what tier before choosing a plan.

Balancing Premium vs. Out-of-Pocket Costs

The relationship between premiums and out-of-pocket costs creates important tradeoffs. Plans with lower monthly premiums typically have higher deductibles and out-of-pocket maximums. Plans with higher premiums usually offer lower cost-sharing when you receive care.

Choosing the right balance depends on your expected healthcare usage. If you rarely need medical care beyond preventive services, a lower-premium plan with a higher deductible may cost less over the year. If you have ongoing health conditions, take regular medications, or anticipate medical procedures, a higher-premium plan with lower out-of-pocket costs often saves money overall.

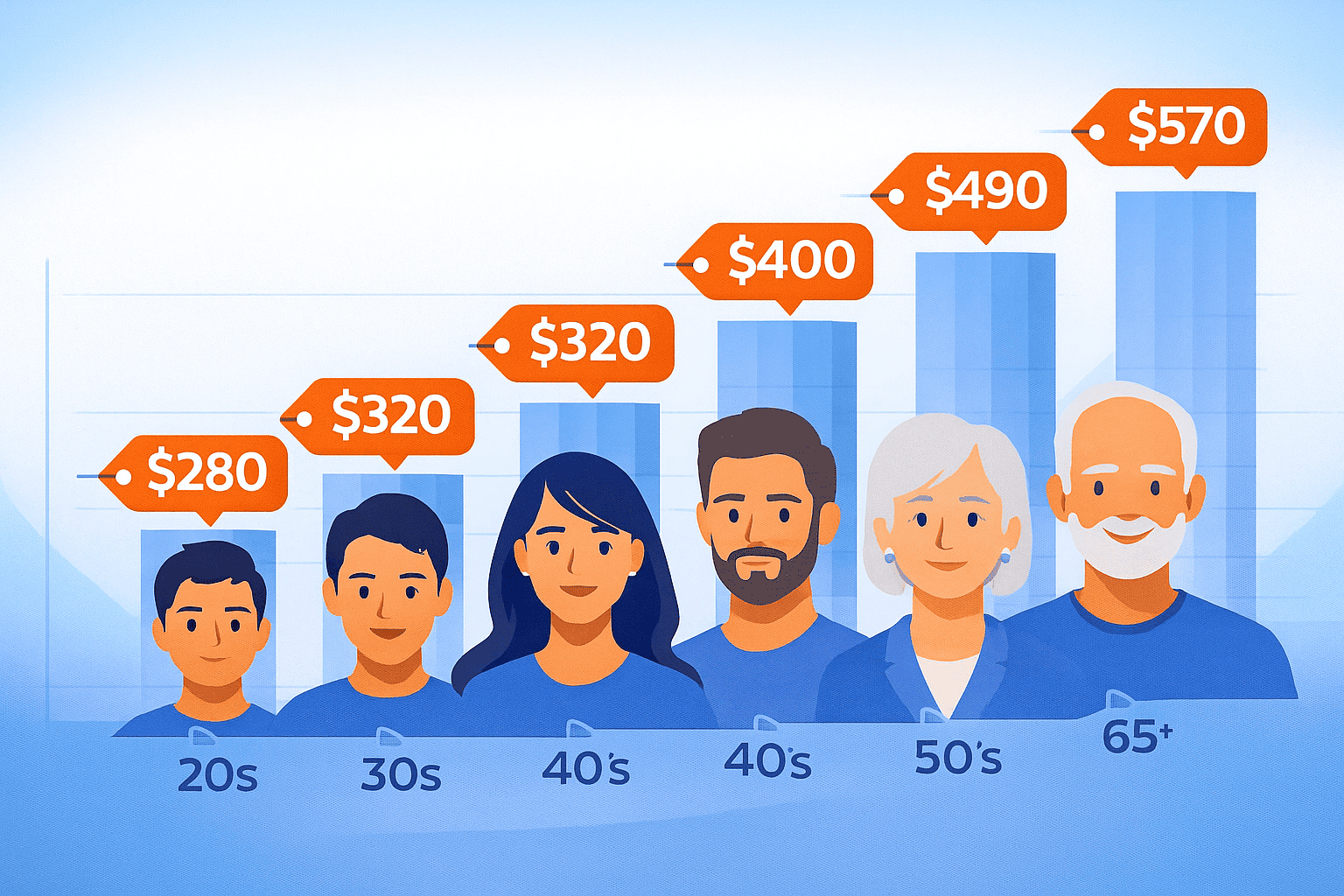

2026 New Jersey Premium Rates by Age

Age is the largest factor affecting premium costs in New Jersey. Under ACA rules, insurers can charge older adults up to three times more than younger enrollees for the same coverage. Here’s what you can expect for Silver-tier plans before subsidies:

| Age Group | Monthly Premium Range | After Typical Subsidy |

|---|---|---|

| 18–25 | $280 – $380/month | $50 – $150/month |

| 26–34 | $320 – $450/month | $75 – $200/month |

| 35–44 | $380 – $520/month | $125 – $275/month |

| 45–54 | $520 – $700/month | $200 – $400/month |

| 55–64 | $750 – $1,050/month | $350 – $600/month |

These ranges reflect 2026 Silver plan averages across New Jersey carriers. Your actual premium depends on your specific location, chosen carrier, and metal tier.

Other Factors Affecting Your Rates

Location

Premiums vary by county based on local healthcare costs and provider availability.

Tobacco Use

Tobacco users may pay up to 50% more. Quitting reduces premiums significantly.

Household Size

Family plans cost more but may qualify for larger subsidies based on total income.

Metal Tier

Bronze costs less monthly; Gold and Platinum have lower out-of-pocket costs.

See Your Actual 2026 Costs with Subsidies

Get personalized quotes showing exactly what you’ll pay after federal and state financial assistance.

Calculate My Premium Call 888-215-4045Premium Tax Credits and Subsidies

Most New Jersey residents qualify for financial assistance that dramatically reduces monthly premium costs. Two programs work together to make coverage affordable: federal premium tax credits and New Jersey’s state-funded Health Plan Savings program.

Federal Premium Tax Credits

Premium tax credits are federal subsidies that lower your monthly payment based on household income. These credits are applied directly to your premium, reducing what you pay each month. Your eligibility and credit amount depend on your income relative to the Federal Poverty Level.

2026 Federal Subsidy Eligibility

- Available to households earning 100% to 400% of FPL

- Single individual: $15,060 to $62,160 annual income

- Family of four: $31,200 to $129,000 annual income

- Credits reduce premiums so you pay no more than a percentage of income

- Take the credit monthly or claim it when filing taxes

New Jersey Health Plan Savings

New Jersey provides additional state-funded subsidies through the NJ Health Plan Savings program. This assistance extends to residents earning up to 600% of the Federal Poverty Level, helping middle-income households who earn too much for federal credits alone.

2026 State Subsidy Limits (600% FPL)

- Single individual: Up to $93,900 annual income

- Couple: Up to $127,380 annual income

- Family of three: Up to $158,580 annual income

- Family of four: Up to $192,900 annual income

- State subsidies stack on top of federal credits for maximum savings

Cost-Sharing Reductions

If your income falls between 100% and 250% of the Federal Poverty Level, you may also qualify for Cost-Sharing Reductions (CSRs). These enhanced benefits lower your deductibles, copays, and maximum out-of-pocket costs. CSRs are only available with Silver plans purchased through GetCoveredNJ.

Income 100-150% FPL

Average deductible: $200

Max out-of-pocket: $2,900

Income 150-200% FPL

Average deductible: $850

Max out-of-pocket: $6,300

Proven Strategies to Save on Coverage

Beyond subsidies, several strategies help you secure quality coverage at prices that fit your budget. Whether you’re shopping for individual coverage or family protection, these approaches can reduce your total healthcare costs.

Choose the Right Metal Tier

Bronze plans work well for healthy individuals who rarely need care. If you have ongoing medical needs, a Gold plan’s lower deductible may save money despite higher premiums. Compare total expected costs, not just monthly premiums.

Consider HMO Plans

HMO plans typically cost 15-25% less than PPO plans. If you’re comfortable using in-network providers and getting referrals for specialists, HMOs offer substantial savings without sacrificing coverage quality.

Use an HSA-Eligible Plan

High-deductible plans paired with Health Savings Accounts offer triple tax advantages: deductible contributions, tax-free growth, and tax-free spending on healthcare. For 2026, contribution limits are $4,300 individual and $8,550 family.

Self-Employed Tax Deduction

Self-employed individuals can deduct 100% of premiums from taxable income. This above-the-line deduction effectively reduces your coverage cost by your marginal tax rate.

Understanding Metal Tiers

ACA marketplace plans are organized into metal tiers that indicate how costs are shared between you and the insurance company. The tier you choose affects both your monthly premium and what you pay when receiving care.

2026 Carrier Rate Changes

Rates vary significantly by carrier. When comparing the best plans, consider that some carriers increased rates more than others:

| Carrier | 2026 Rate Change | Notes |

|---|---|---|

| Oscar | +4.6% | Lowest increase; technology-focused plans with strong digital tools |

| AmeriHealth | +13.5% | Strong networks in Central and South Jersey regions |

| Horizon BCBS | +17.0% | Largest statewide network with most provider options |

| Ambetter | +17.2% | Budget-friendly options; growing network coverage |

| UnitedHealthcare | +18.4% | National carrier with strong out-of-state coverage |

These rate changes reflect each carrier’s claims experience, network costs, and assumptions about the 2026 enrollment mix. A carrier with a higher rate increase isn’t necessarily more expensive overall. Oscar’s lower increase, for example, started from a different baseline than other carriers. Comparing actual premium quotes for your age and location provides the most accurate picture.

Note: Aetna exited the New Jersey marketplace for 2026. If you previously had Aetna coverage, you’ll need to select a new carrier. The remaining five carriers offer comparable plan options across most of the state.

Shopping During Open Enrollment

Plan options and prices change annually. Even if you’re satisfied with your current coverage, reviewing alternatives during open enrollment can reveal better options. A plan that was the best value last year may not be the most competitive choice for 2026.

The 2026 open enrollment period runs from November 1, 2025 through January 31, 2026. Enrolling by December 31 ensures coverage starts January 1. Those who enroll by January 31 receive coverage starting February 1. Outside open enrollment, you can only enroll if you experience a qualifying life event such as losing other coverage, getting married, having a child, or moving to a new area.

See How Much You Could Save

Financial assistance can significantly reduce what you pay for coverage. See your actual costs after federal tax credits and New Jersey state subsidies.

Calculate My Savings Call 888-215-4045New Jersey Health Insurance Costs FAQ

How much does health insurance cost in New Jersey without subsidies?

Without subsidies, monthly premiums range from about $280 for young adults to over $1,000 for those approaching age 65. The average unsubsidized Silver plan premium is approximately $550–$650 per month for a 40-year-old. However, most New Jersey residents qualify for financial assistance that significantly reduces these costs.

What income qualifies for health insurance subsidies in New Jersey?

Federal premium tax credits are available to households earning between 100% and 400% of the Federal Poverty Level. For 2026, that equals $15,060–$62,160 for individuals and $31,200–$129,000 for a family of four. New Jersey’s state subsidies extend assistance up to 600% FPL, allowing individuals earning up to $93,900 and families of four earning up to $192,900 to qualify.

Why did New Jersey health insurance rates increase for 2026?

Rates increased an average of 16.6% due to rising healthcare costs, higher utilization, and increasing prescription drug expenses. The expiration of enhanced federal premium tax credits at the end of 2025 also affected pricing. Carriers additionally priced in expectations that some healthier enrollees may drop coverage due to higher premiums.

How can I reduce my health insurance costs in New Jersey?

You can lower costs by applying for subsidies through GetCoveredNJ, choosing an HMO instead of a PPO if network limits work for you, selecting a Bronze plan if you rarely use care, using an HSA-eligible plan for tax advantages, and comparing carriers since rate changes vary widely. Self-employed individuals may also deduct premiums from taxable income.

What’s the difference between premium costs and out-of-pocket costs?

Your premium is the monthly amount you pay to keep coverage active. Out-of-pocket costs include deductibles, copays, and coinsurance when you receive care. Plans with lower premiums typically come with higher out-of-pocket costs, while higher-premium plans usually reduce cost-sharing when services are used.

When is open enrollment for 2026 New Jersey health insurance?

Open enrollment for 2026 coverage runs from November 1, 2025 through January 31, 2026. Enroll by December 31 for coverage starting January 1, or by January 31 for coverage starting February 1. Outside this window, enrollment is limited to qualifying life events such as losing coverage, marriage, or the birth of a child.

New Jersey Health Insurance Resources

Compare personalized rates with real-time subsidy calculations.

Marketplace GuideNavigate GetCoveredNJ enrollment and subsidy eligibility.

Best PlansSee top-rated carriers with detailed coverage analysis.

Individual CoverageExplore options for individuals and families in New Jersey.

Self-EmployedTax deductions and coverage solutions for business owners.

All NJ PlansComplete guide to health insurance options in New Jersey.

Find Affordable Coverage for Your Budget

See exactly what you’ll pay for New Jersey health insurance after all available subsidies. Our licensed specialists calculate your federal tax credits and state assistance to show your true cost.

Get My Cost Estimate Call 888-215-4045Licensed in New Jersey • Same prices as GetCoveredNJ • Free consultation

Independent Broker Notice

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.